CHN: House Tax Cut Bill Heads Towards Floor Vote; Senate Releases Its Version

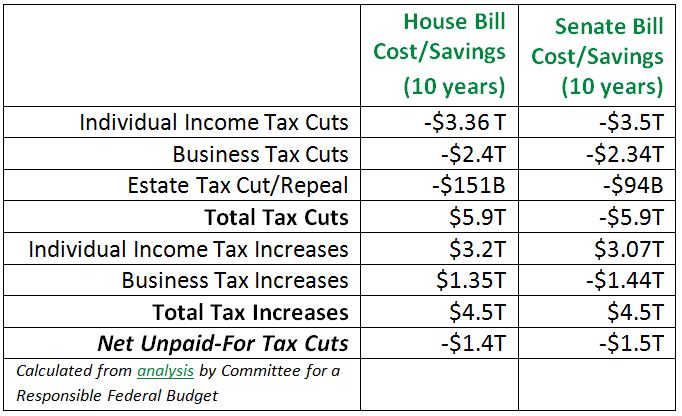

The House Ways and Means Committee completed its markup of H.R. 1, the Tax Cuts and Jobs Act, and passed the bill (24-16 along party lines) on Nov. 9. The full House is expected to vote on the bill the week of Nov. 13. The bill would provide trillions of dollars in tax cuts, overwhelmingly to the wealthy and corporations, and would add $1.4 trillion to the U.S. debt over the next decade. An analysis of the House bill by the Institute on Taxation and Economic Policy (ITEP) found that not only would the wealthiest 1 percent receive the greatest share of the total tax cut in its first year (31 percent, for an average tax cut of $48,580 in 2018), but that their share would actually grow over time, reaching 48 percent by 2027 (for an average tax cut of $64,720 per person). Tax cuts for those at the middle and lowest end of the income scale would be significantly lower (an average cut of a little more than $14.40 a week and $2.50 a week, respectively, in 2018), and these would drop over time. The bill makes harmful changes to the Child Tax Credit to exclude immigrant families, harming 1 million immigrant children; see the related article in this Human Needs Report for more information. A few changes were made to the bill during committee action, including a provision that would make it more difficult for small business owners or those who are otherwise self-employed to claim the  Earned Income Tax Credit and increase their chances of being audited for tax deductions they did not claim. The bill also originally called for a repeal of the adoption tax credit, but this provision was removed. For more information on the House tax cut bill, see the Nov. 3 edition of the Human Needs Report and CHN’s blog.

Earned Income Tax Credit and increase their chances of being audited for tax deductions they did not claim. The bill also originally called for a repeal of the adoption tax credit, but this provision was removed. For more information on the House tax cut bill, see the Nov. 3 edition of the Human Needs Report and CHN’s blog.

The Senate Finance Committee released its vision for tax cuts on Nov. 9 as well. While certain provisions differ from the House bill (more on this below), the Senate version is similar to the House bill in that it gives trillions of dollars in tax cuts, disproportionately to the wealthy and big corporations, and adds nearly $1.5 trillion in debt over 10 years. While there are some tax cuts for middle class families, some will actually see increases, similar to the House bill.

Timing: The Senate Finance Committee is expected to take up the bill beginning the week of Nov. 13. The full Senate is expected to vote on it the week of Nov. 27, after the congressional week-long Thanksgiving break. Because the Senate is using a special process known as reconciliation to move this bill, as provided in the budget resolution, only a simple majority is needed to pass the Senate rather than the usual 60-vote threshold. If tax cut bills pass in both chambers, they must work out the differences between the two. House and Senate leaders aim to have a bill on President Trump’s desk before Christmas. However, as many parts of the bill are controversial, the schedule could slip or stall.

Impact on Individuals: The congressional Joint Committee on Taxation has released estimates of the cost and total revenue changes by income groups for the Senate plan, but other analyses with more detail about gains or losses are not yet done. Here is what is known so far:

Tax Rates: The Senate plan keeps seven tax brackets, similar to current law, but with cuts in most of the rates. The top rate, currently 39.6 percent, would drop to 38.5 percent, and the bottom income level for this bracket would rise from $470,700 for joint filers to $1 million. This would be favorable to those with high incomes, since more of their income will now be taxed at a lower rate. The lowest tax bracket would stay at 10 percent. This structure is different from the House bill, which consolidated the brackets to just four (raising the lowest bracket’s tax rate to 12 percent and keeping the rate for the highest bracket at 39.6 percent).

Deductions/Exemptions: Similar to the House bill, the Senate plan roughly doubles the standard deduction, to $12,000 for single individuals and $24,000 for married couples.

Child Tax Credit/Earned Income Tax Credit/American Opportunity Tax Credit: The Senate plan increases the Child Tax Credit from $1,000 per child to $1,650 (vs. $1,600 in the House bill). The credit will be available for children under age 18 (current law provides the CTC for children under 17). Families with incomes of up to $500,000 will be able to qualify for the full Child Tax Credit, with a reduced credit available until it phases out at $1 million for 2-parent families (vs $230,000 in the House plan). The threshold for the refundable part of the Child Tax Credit would drop to $2,500 in earned income, from $3,000. The Senate bill would create a new non-refundable $500 credit per non-child dependent. The Child Tax Credit is changed to deny the benefit to about 1 million children in immigrant families, by requiring all children claiming the credit to have Social Security numbers. Most children in immigrant families are citizens, but about 1 million are “Dreamers,” brought here at a young age. The Dreamers would lose the CTC under this proposal. Under current law, immigrant parents who pay taxes through the use of an Individual Taxpayer Identification Number (ITIN) can receive the CTC for their children.

Repeal of Other Tax Credits and Deductions: The Senate plan retains a credit for families that adopt a child (the House initially proposed to terminate the credit, but restored it before the tax bill was approved in committee). It also retains deductions that would have been eliminated in the House bill, such as deductions for medical expenses, student loan interest, and teacher expenses. The mortgage interest deduction, which is reduced in the House bill, is retained in the Senate bill.

State and Local Tax Deduction: The deductions for all state and local taxes, including income, sales, and property taxes are eliminated. In the House bill, taxpayers may still deduct their property taxes up to a total of $10,000. There has been strong opposition to these changes for their effect on states with higher state and local taxes, both because of the tax increase that families will experience and the losses in revenue anticipated in states and local communities that will affect schools, public safety, and transportation, and many other services.

Alternative Minimum Tax: Similar to the House bill, the Senate plan would repeal the Alternative Minimum Tax. This has been in place to ensure that high-income individuals cannot utilize deductions sufficient to wipe out all their tax obligations. In the one tax return made public by President Trump, he paid $31 million because of the Alternative Minimum Tax. Eliminating it provides a tax break of $695.5 billion to upper-income individuals.

Estate Tax: Under current law, estates from individuals are exempt from the tax if they are worth less than $5.5m (or $11.2 million for couples). The exemptions would double under both the House and Senate bill; The Senate bill would not eliminate the estate tax, as the House bill would do in 2024. The estate tax change would leave less than 2,000 estates nationwide subject to the tax.

Corporate/Business Taxes: Corporate tax rates would decline from a maximum 35 percent to 20 percent beginning in 2019 (vs. 2018 in the House bill, a tax break for corporations of nearly $1.5 trillion). The Senate plan would create a 17.4 percent deduction for unincorporated businesses (such as partnerships) that pay taxes through the individual income tax, meaning the top tax rate for such “pass-through” income would be 31.8 percent rather than 38.5 percent for the first $150,000 of such income. The Trump Organization is said to include about 500 such “pass-through” businesses in Donald Trump’s individual tax returns. There would also be favorable treatment of businesses sheltering income in overseas tax havens. In order to gain short-term revenue, companies with foreign income would have to pay a one-time 10 percent tax, which would bring in $190 billion (far less than the $750 billion such companies actually owe on their offshore holdings). The Work Opportunity Tax Credit (a tax break for employers who hire low-income workers, worth $3.6 billion), and the New Market Tax Credit, which incentivizes investment in distressed communities, are retained in the Senate bill; both are repealed in the House plan. A credit for clinical testing expenses for drugs for rare diseases (worth $54 billion) that is eliminated in the House bill is reduced but not eliminated in the Senate bill.

Non-profit Organizations: There are no changes in the Senate bill to the Johnson Amendment, which currently prohibits churches and non-profits that are tax-exempt under IRS rules from supporting or opposing candidates for public office. The House bill would significantly weaken the Johnson Amendment, opening the door to churches engaging in electoral activity. Many non-profits oppose this change, believing it will lead to a lessening of trust in these institutions and ultimately reduce their support. In addition, although the charitable deduction is retained, fewer taxpayers will itemize because of the increase in the standard deduction. Non-profits worry that this will reduce the number of donations. One estimate is that taxpayers with incomes below $280,000 will not find it advantageous to itemize, and therefore will not have the tax incentive to make charitable contributions.

Affordable Care Act individual mandate repeal: The White House and some conservatives are pushing for the tax cut bill to also repeal the individual mandate of the Affordable Care Act, which requires that all individuals obtain health insurance or pay a penalty. While neither the House nor Senate bill contain this provision, it could potentially be added as an amendment on the Senate floor or when the two chambers work out a compromise bill.

The Upshot: Similar to the House bill, the wealthy and corporations will be the biggest beneficiaries of the Senate tax cut plan. Advocates are fighting hard against both the House and Senate tax cut bills, calling them a one-two-three punch inflicted on low- and middle-income Americans. First, people are hurt in the near-term by seeing their taxes go up from the loss of deductions or credits; the bills eliminate many deductions and credits low- and middle-income families rely on, including (in the House and/or Senate versions) the medical expense deductions, certain college deductions and credits, state and local income and sales tax deductions, and the Child Tax Credit for immigrant families. Up to 1 in 4 middle-class families will pay more taxes under the House GOP tax plan by the tenth year. In fact, one estimate that looks specifically at families with children under 18 finds that more than 40 percent of them will pay higher taxes in 2027. Next, larger deficits created by these bills will be used as an excuse to cut domestic programs and services Americans rely on, such as Medicaid, SNAP, education, housing, and others. These cuts will come on top of years of cuts sustained by some of these programs. Finally, some tax changes that could have been used to invest in real national priorities, such as using the money saved by reforming the mortgage interest deduction to increase affordable housing for low-income families, will instead be given to the rich and wealthy corporations.

Subscribe: