Who’s hurt by payday lending?

Editor’s note: CHN Intern Bridget Rittman-Tune is a senior at the University of Maryland, College Park. She is studying Women’s Studies and Geographic Information Systems.

It is well known that the payday lending industry targets the most vulnerable among us. Particularly vulnerable are African Americans, victims of domestic violence, and veterans as well as active members of the military.

It is well known that the payday lending industry targets the most vulnerable among us. Particularly vulnerable are African Americans, victims of domestic violence, and veterans as well as active members of the military.

The Trump Administration is pushing to roll back an Obama-era rule that would protect consumers from predatory payday and car title lenders. Before they can do that, staff must take into account comments from the public. CHN and many of our allies are working to generate comments opposing this rollback and you can voice your opposition here. We will also be hosting a webinar on this topic on Thursday, May 2 at 2 p.m. ET. Register for the webinar.

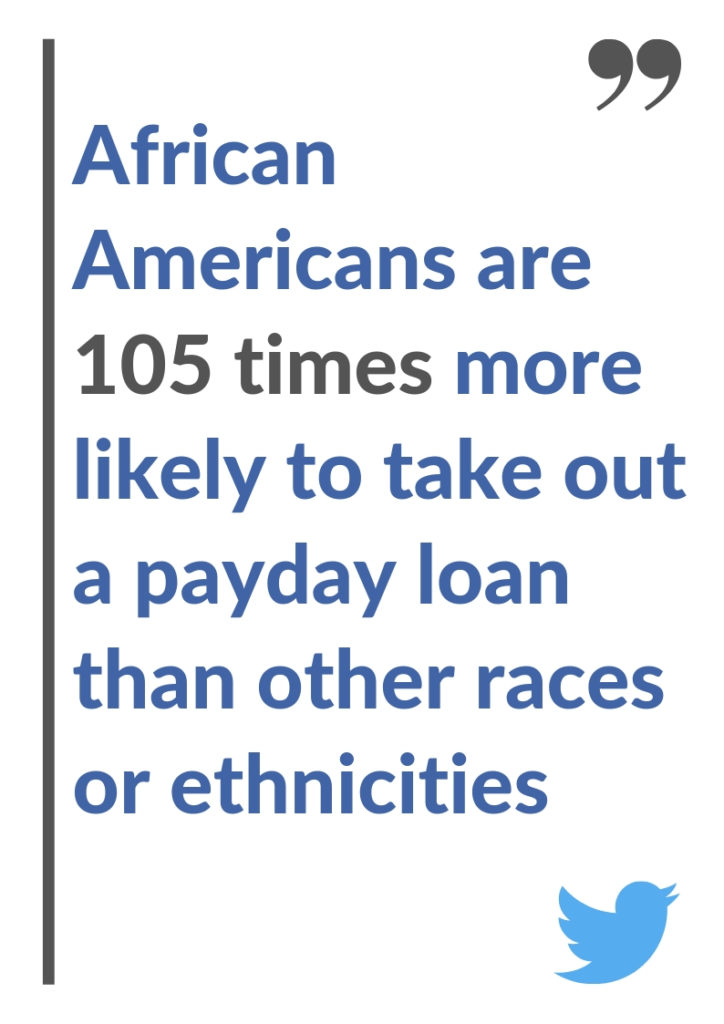

So, how is payday lending hurting African Americans, victims of domestic abuse, veterans and active members of the military? African Americans are clearly being targeted because they are 105 times more likely to take out a payday loan than other races or ethnicities; research shows a mostly black neighborhood is more likely to have payday lenders than a mostly white neighborhood, even when income, density, and homeownership are the same.

Economic control is one of the main threats used to keep domestic violence survivors from escaping their situation. Payday lending is structured so that borrowers become dependent on repeat loans and this is even more harmful to survivors of domestic violence, because they are seven times more likely to live in low-income households and 99 percent of survivors already experience economic abuse at the hands of an intimate partner. Domestic violence survivors have had to turn to predatory loans when factors like poverty and unemployment block their access to mainstream banking options. The Consumer Financial Protection Bureau found that the median payday-loan borrower spent 199 days per year in debt. This is especially dangerous for domestic violence survivors who might then be forced to stay in violent situations or risk the uncertainty and violence that comes from becoming homeless. Economic hardship is the main reason survivors return to abusive relationships.

The Center for Survivor Agency & Justice talked with Jane, a survivor from St. Louis, MO, who “experienced financial challenges when she left an abusive relationship. Because her safety net had been depleted as a result of the abuse, she took out payday loans in order to pay creditors and to keep her utilities on, despite the astronomical interest rates. Soon Jane was unable to repay the loans, was desperate for cash, and afraid for her safety. She teetered on the edge of eviction and bankruptcy.”

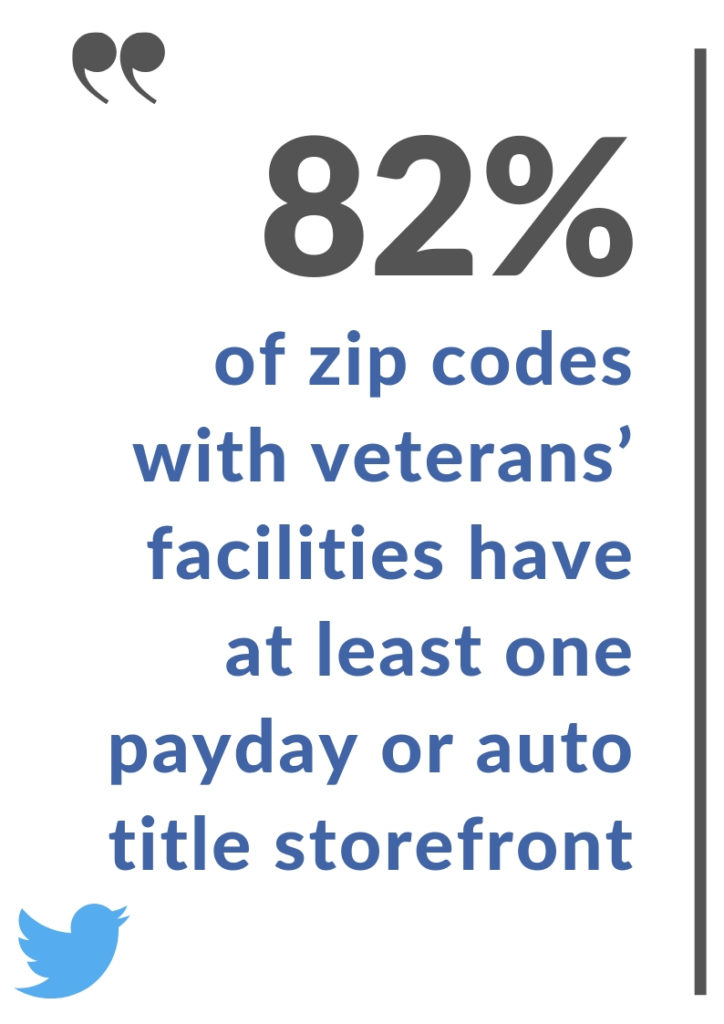

U.S. Veterans use payday loans at a rate that’s nearly four times the national average. These loans often increase financial hardship for veterans, which is of such serious concern because 1.4 million veterans are at risk of homelessness. In Texas, 82 percent of zip codes with veterans’ facilities have at least one payday or auto title storefront and almost 50 percent have five or more payday loan storefronts.

U.S. Veterans use payday loans at a rate that’s nearly four times the national average. These loans often increase financial hardship for veterans, which is of such serious concern because 1.4 million veterans are at risk of homelessness. In Texas, 82 percent of zip codes with veterans’ facilities have at least one payday or auto title storefront and almost 50 percent have five or more payday loan storefronts.

Robert Chaney, a 66-year-old veteran from Boise, lives off of Social Security benefits, but borrowed from an Internet payday lender last November after his car broke down and he didn’t have the $400 for repairs. When the 14-day loan came due, he couldn’t pay, so he renewed it several times. He ended up taking out multiple loans from multiple sites, trying to stave off bank overdraft fees and pay his rent. Eventually, payday lenders — who had direct access to his checking account as part of the loan terms — took every cent of his Social Security payment, and he was kicked out of his apartment. He had borrowed nearly $3,000 and owed $12,000. “I’m not dumb, but I did a dumb thing,” said Chaney, who is now homeless and living in a rescue mission.

Payday lenders target service members and their families at twice the rate that they target civilians. These problems have wide-reaching consequences. When service members become overwhelmed with debt and high-cost loans it becomes an issue of military readiness. Ramifications of service members’ debt to payday lenders are loss of security clearances and distraction from work due to such crushing financial stress. In some cases service members have been kicked out of the service because their financial situations became so disastrous.

Navy Petty Officer 2nd Class Jason Withrow, who is stationed at a naval submarine base in Georgia, took out a payday loan to make ends meet after being hurt in a car wreck. A back injury had forced him to drop his second job loading beer kegs at the Navy exchange. Withrow soon found himself taking out loans with other payday lenders to pay the interest on his initial advance. In five months, I spent about $7,000 in interest and didn’t even pay on the principal $1,900,” said Withrow, 24, of Brooklyn, Mich. “I was having marital problems because of money and didn’t know what to do for Christmas for my kid.”

If you think that consumers deserve more protection from the payday lending industry and not less, go here and leave a comment.

Subscribe: